THE NORTH CAROLINA RETIREMENT SYSTEM AND YOUR PENSION - PART II

THE NORTH CAROLINA RETIREMENT SYSTEM AND YOUR PENSION - PART II

INVESTMENT ADVICE IS NOT CHEAP

Treasurer Boyles’ investment world in 1977 was a lot simpler than now. His $40 billion fund paid advisory fees of about $50 million, a rate of $.13 on every $100 invested. This low rate was possible because much of the investment was in bonds that have lower advisory fees than stocks.

By 2010, the search for higher investment returns dictated that the fund invest in assets besides stocks and bonds. It added hedge funds, private companies, real estate, timber, and natural resources. The legislature’s pension committee reviewed and approved guidelines for each type.

The pension fund has two categories of asset management, those for which outside advisors make the investment decisions and those managed by an internal staff at the Treasurer’s Department. The internal funds are at a far lower cost.

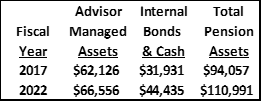

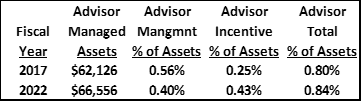

In 2017, the fund had grown to $94 billion. The investments became more complex with more advisors. Base fees were $346 million and incentive fees to the advisors for exceeding a benchmark return were $153 million. This total cost was now $.80 per $100 on the $62 billion managed by outsiders.

Investment advisory fees, paid to outside advisors, are a necessary and large expense for a giant pension fund. The fee structure is often confusing to outsiders. Treasurer Folwell addressed the fees when he took office. But changes did not come easily. He was locked into some investment commitments. But he moved $15 billion from outside advisors to a new internal stock fund, pruned the number of outside advisors, and negotiated lower fees.

Over the last five years, the internal funds have increased from 34% to 40% of total fund assets. This shift to internal management has reduced costs by $60 million a year. (All the data presented below are in millions of dollars).

The fund still had 197 investment advisers investing in 283 separate funds. Even as the fund has grown in the last 5 years, the advisory fees have been reduced from .56% to .40%, a cost savings of $104 million.

Some advisors have an incentive fee if they make a return greater than a benchmark. The treasurer cannot control these fees. They depend on how well the managers perform each year. Fiscal year 2022 was far better than 2017. Base fees were lower. Incentive fees were higher because of good performance.

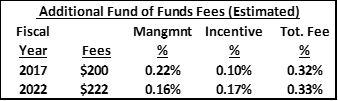

Investments incur yet another layer of fees because some managers hire subadvisors who also have advisory fees and incentive fees. These costs are not reported directly but are reflected in the net return that the advisors report. Such fees may be $200 million. A fair estimate is that the management fee for subadvisors has been reduced from .22% to .16% over the last five years, giving a savings of $80 million.

Treasurer Folwell has cut annual costs well over $200 million. He is locked into some investments that he inherited, but over time he may reduce these expensive relationships. The bill for all fees is estimated at over $700 million.

There is still room to improve the number and type of investment managers and their fees. Perhaps Folwell’s staff can manage more of the money ‘in house.’ The fund should also be able to negotiate lower advisor fees, given its size.

These fees are significant. At $700 million annually, the fees cost every North Carolina family $225 a year. A cost borne, even if indirectly, by all the people in the state. The $200 million cut in fees has saved each family $65 a year.

On my report card for managing fees, the Treasurers get a grade somewhere between C- and A-, depending on the action each Treasurer has taken.

OVERALL PERFORMANCE

Treasurer Folwell has made real progress with the pension fund. His investment fee reduction of over $200 million, compared to the cost structure in 2017 is not the whole story.

The fund is compared by an outside consultant to a peer group of 14 similar sized public funds. The relative performance compared to this group is even more impressive than the amount of dollars saved.

The base investment fee rate is less than half that of the peer average for the total (outside and internal) assets. The return is slightly below the return of the peer group, but offsetting that – the risk for the fund’s asset mix is also lower. The general administration of the fund runs only 35% of the cost of the peer group, a saving of $9 million a year.

CHALLENGES TO KEEPING THE PENSIONS SAFE

Many factors determine whether a fund is sound. Some are within the control of the Treasurer and the legislature and others are not but keeping the fund on track is a heavy responsibility. The last four Treasurers have made tough choices. I give them a collective ‘A’ because they did what they had to do.

Until 1981, interest rates were 7-8%. If the fund had a 7.5% funding rate, it could beat this goal mostly with bonds. From 1976-2000, the fund made 11.2% a year with little risk. The funding level was 110%, more money than was actuarially required.

But the investing world changed in 1981. For the next 20 years, the stock market earned only 7.4% a year. And interest rates declined for 40 years. The Treasurers had to buy more stocks to meet the actuarial target. The stocks’ volatility meant that the fund took on more risk – a bigger chance that it might do poorly.

Changing the actuarial funding rate 1/10th of 1% changes the funding level by 1.0%. When the Treasurer cut the actuarial rate from 7.0% to 6.5%, the funding level dropped from 95% to 90%, about $6 billion. This puts the legislature on notice that Folwell needs more money to build the fund back to 95% or more. The legislature decides where the money will come from, and how soon. They naturally tend to defer funding as long as possible, hoping that the investments will earn more. Nobody wants to deliver the news of a tax increase.

THE EARNINGS RATE’S IMPACT

The actuarial funding rate is a key component in measuring the fund’s ability to meet its obligations. And it is critical that the fund earns at least that 6.5% return.

But this rate cut puts the legislature on notice that making money is going to be more difficult, and the state’s contribution may need to increase. Typically, those who levy taxes want tax cuts, not increases. Voters naturally reward them when they promise lower taxes, and if the promise is not met, the politician may be gone before the failure is apparent. And whoever replaces them can say, “I inherited this mess. It isn’t my fault.” Often a never-ending cycle of neglect and excuses.

Lawmakers can argue that they need the money for other things now; that funding can be postponed, and the stock market will surely go up and fill the shortfall. Fortunately for North Carolina, the Treasurer and legislature have worked together to address this problem realistically. While their work has not been easy, the high rank for the North Carolina fund speaks to their cooperation.

THE PENSION PLAN BENEFIT

The employees’ pension benefit is generous. What you put in and how long you work determine what you draw out. Options allow you to retire early at a lower monthly pay for life or to allow your spouse to get payments at your death.

You deposit money in the fund and your employer matches about $2.00 for every $1.00 you put in. The fund invests this money, and it grows until you retire. Then you receive a monthly check for life based on what you earned at the end of your employment and how many years you worked.

For example - You begin work paid $40,000 a year, work for 30 years with pay increases of 3.5% a year. At retirement, you will receive a yearly pension of $53,000, half of final pay. The benefit stops at death. So, the longer you live, the better deal the pension is. With a life expectancy of 20 years after retirement, the pension pays out a return of about 7% on the money you put in.

If you withdraw from the plan, you get back all the money you invested plus 4% interest. Withdrawing usually does not make sense. Most people will not make a higher return than the fund will.

Coming Soon – Part III: Social Security and state plans; Supplemental plans; Looking forward and getting involved.

Great morning Gene,

As you no, I had the great pleasure of having a ear around investment talk for twenty years.

I have to kindly admit that your post has taught me much more in a few months than I ever knew.

The lesson’s on: Advisors, Sub-advisors, management fees, the turn around in 1981 and more!

I would have loved to have been a part of The Pension Plan Benefit crowd, that was a plus.

Keep up the great teaching Gene,

Stay well.

Patrice