TOBACCO STOCKS – A GOOD INVESTMENT?

TOBACCO STOCKS – A GOOD INVESTMENT?

INTRODUCTION

Many readers of these posts are security analysts. For them, the values of tobacco stocks range from important to critical. For those of you who are not analysts, this post will give you a taste of how difficult security analysis and forecasting are. You can even try your hand at forecasting. But I’m getting ahead of myself.

In a May 17 post, I discussed how tobacco stocks had performed well in the market selloff since late 2021. Many readers have said that they own tobacco stocks and think they are a sound investment. As the market has declined, they have been correct.

These tables are updates of the ones presented on May 17.

The S&P 500 has increased 3% since the May 17 post, but tobacco stocks as a group have fallen 9%. The tobacco stocks have still done significantly better than the market since bottoming in October 2021.

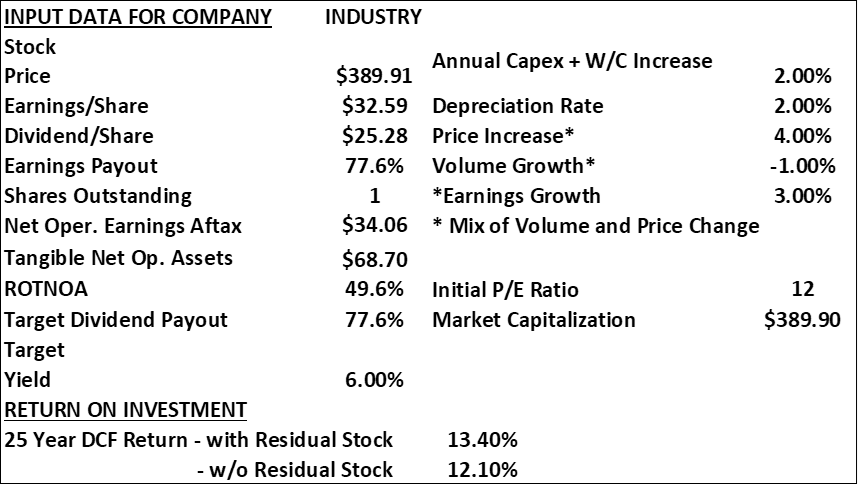

TOBACCO INDUSTRY – OPERATING HISTORY

For the last 60+ years, tobacco companies have been remarkably consistent in their business operations. They have had:

An oligopoly with limited competition from new entrants

A loyal but declining customer base

Almost unlimited pricing power

Low labor content in the product

Low marketing costs – due to advertising prohibition

An exceptional return on tangible net operating assets

But they have also had:

Threats from anti-smoking campaigns and ever-increasing taxes

Stakeholders (beyond shareholders) who derive $ billions in annual benefits

ANALYSIS METHODOLOGY

I know far less about tobacco stocks than skilled professional analysts who follow the industry. But I have put together an analysis of what I think a tobacco company must do to be attractive as an investment for the long term. (Note that this is not a forecast of what I believe they will do.)

This table combines the six major tobacco companies in an industry group as though it were a fund with all of them at their market weighting.

These stocks have similar operating results:

High Dividend Payouts as a percent of earnings: (78%)

High yields as a percent of price: (6.5%)

Exceptionally high return on Net Operating Assets: (50%) NOA: Plant, Equipment, Inventory, and other working capital necessary to operate. Operating Earnings are the after-tax earnings from operations with no consideration for debt on the balance sheet or the value of non-tobacco businesses.

The tobacco companies also have common operating themes that are not quantified:

Low marketing and R&D costs

Little need for new plant and equipment, except for replacing existing facilities

Challenges on the health issues with tobacco.

Declining unit volume

Opinions on the future of tobacco range from;

Pessimistic – a major decline in unit sales to Optimistic – new profitable “growth” products to replace cigarettes.

My analysis assumes that the tobacco companies will operate for the next 25 years in much the same way they have since 1960. They will maintain operations with minimal new expenditure, generate great cash flow and use the cash to pay dividends and buy back stock:

Volume will shrink 1% a year,

Price increases will be 4% a year.

The depreciation rate of assets will be 2% a year.

Asset investment will be 2% a year.

The stock will be priced to give a 6% yield.

73% of net earnings will be paid out in dividends.

Remaining net cash flow will buy back shares of stock.

In this scenario, the discounted cash flow return for the industry would be 12.1% at the end of 25 years, giving no value to the residual stock. If the value of the residual stock is included, 13.4%. This return is consistent with the way tobacco stocks have behaved for the last 120 years. My analysis assumes that the industry will survive for another 25 years in much the same form it has today. If external pressures, governmental or health, forced the industry out of business during the 25 years, then the expected return would be lower. However, Tobacco appears to be in no greater danger of extinction than has been the case since 1960.

But the future may not be like the past. The attached spreadsheet will allow you to input your own assumptions about the future of the industry and any of the six individual stocks. [LINK to spreadsheet]You can download the excel file [i] and then put in your own estimates. The Data tab shows the current data for each company and the industry. The spreadsheet allows you to put in data for the industry or for each company, using your own forecast for any of the data in red. (For example, if the price of the “industry” declined 10%, the return would increase to 14.6% and 12.4% when buying at the lower price. Or if tobacco product prices increased 6% annually rather than 4%, the return would be 15.6% and 14.3%.)

I hope this tool will help you understand the key elements in valuing tobacco companies. For those of you who are not professional analysts, but are mathematically inclined, I urge you to try some estimates of your own. You will be surprised how changes that seem minor can impact the expected return.

You will better appreciate the difficult job professional analysts have. Not only is there a great range of possible outcomes for the variables listed, but a host of others are lurking out there, as yet unknown. Some will be good, and some will be bad. Investing is never easy. [ii] [iii]

“The future ain’t what it used to be.”

Attributed to Yogi Berra

[i] Download using: File>Download>Microsoft Excel

[ii] Devin LaSarre is an interesting analyst who has done work on the valuation of the tobacco industry. Those interested in tobacco as an investment should follow Devin’s website, [INVARIANT]. On June 13, he wrote an outstanding analysis of Altria (Philip Morris USA). It is one of the most complete research reports I have ever seen, even though Devin is a “self-taught” financial analyst with no formal training. He has done follow-up work on the outlook for the industry in general, and Altria specifically. His reports are well worth following. You might like to compare his outlook for Altria with the result using the model in this report.

[iii] Chris Pavese, at Broyhill Asset Management gave a fine presentation about Philip Morris International at a conference, You can see it [HERE].

Another fantastic piece - I especially appreciate your ability to filter out the extraneous and distill key information. I'm going to have some fun tinkering with the spreadsheet provided.